What's Included?

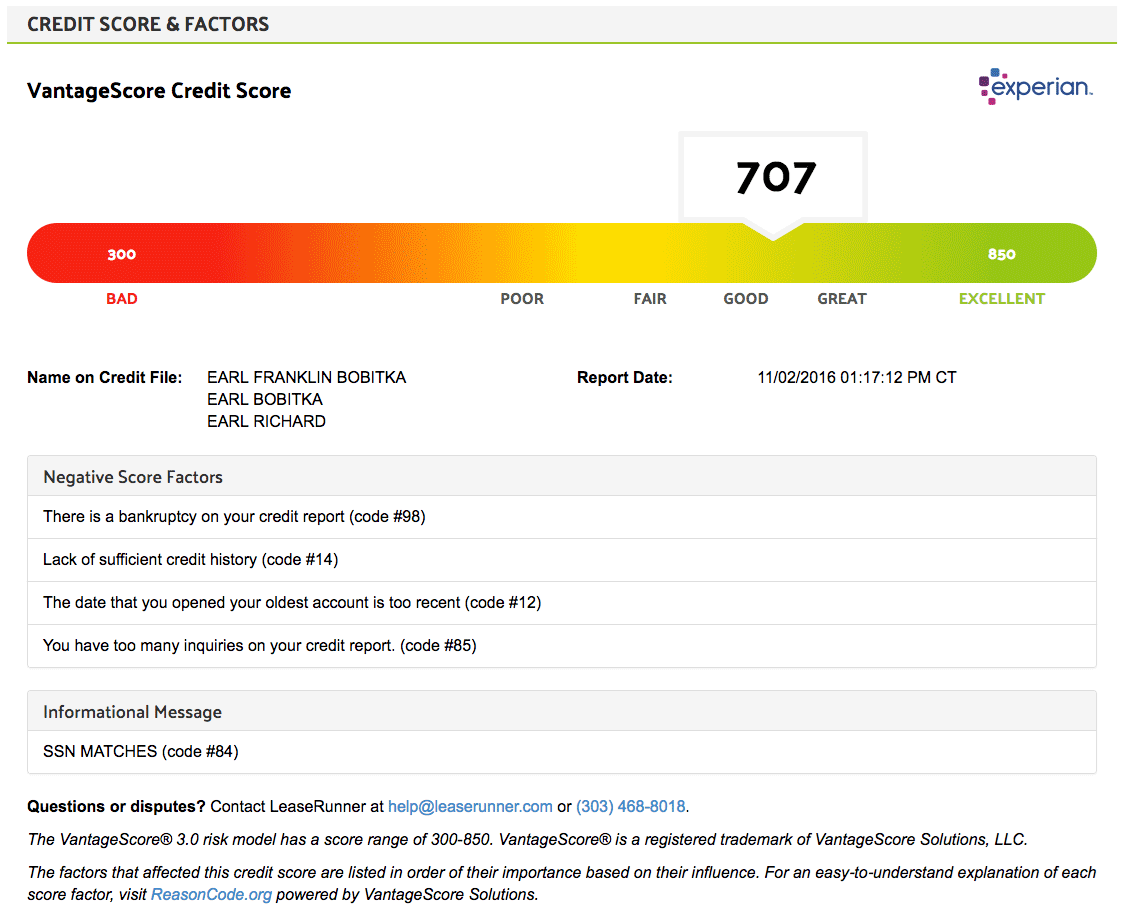

How Is The VantageScore 3.0 Calculated?

Based on tenant's credit reports, landlords prefer tenants with a VantageScore over 650, as it signifies financial reliability and a lower risk of late payments or defaults. The score is determined by financial factors such as:

Payment History

Age and Type of Credit

Credit Utilization

Total Balances and Debt

Recent Credit Behavior/Inquiries

Available Credit

Benefits

VantageScore 3.0 for Landlords & Property Owners

Reduce financial risks by screening tenants based on an advanced, data-driven credit score that predicts future credit behavior, ensuring stable, long-term tenants.

Inclusive of New Credit Users

VantageScore is useful when evaluating new-to-credit applicants, allowing landlords to welcome a wider range of tenants overlooked by traditional scoring models.

Forecasting Payment Risks

VantageScore is designed to better predict future financial behavior, assisting you with an edge in making well-informed decisions that reduce risks.

Non-Invasive to Credit Score

VantageScore 3.0 uses a soft inquiry, meaning no impact on the tenant's credit score—unlike traditional systems that may trigger a hard inquiry.

Our Offerings

Pricing Plans

Pay-as-you-go and decide who covers the fees, with complete transparency in pricing.

Basic Screening

$17/per applicant

*Paid by applicant or landlord.

Pro Screening

$40/per applicant

*Paid by applicant or landlord.

Ultimate Screening

$54/per applicant

*Paid by applicant or landlord.

Most popular

Premium Screening

$64/per applicant

*Paid by applicant or landlord.

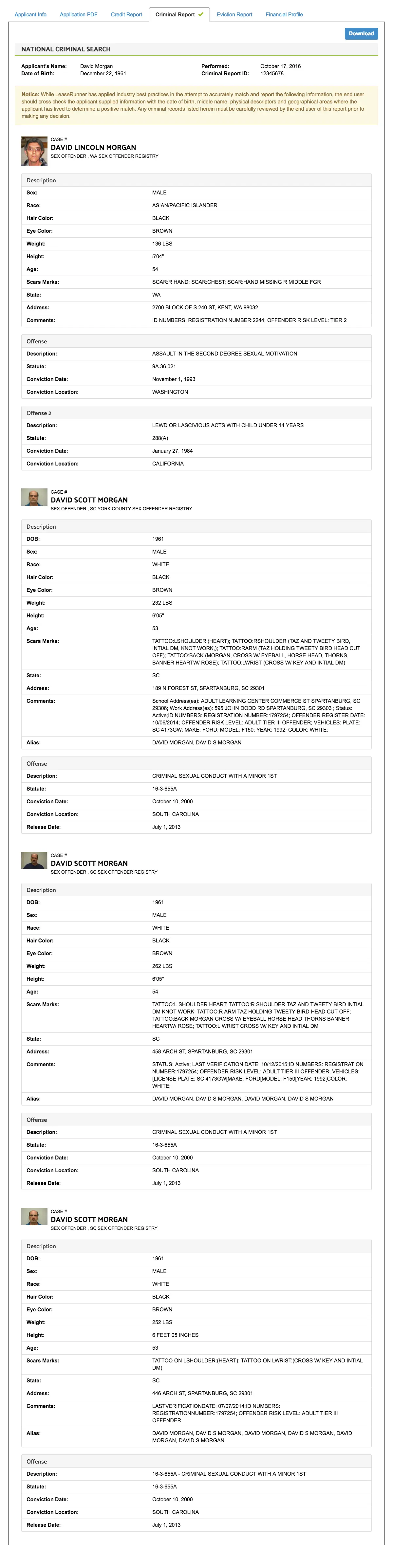

Criminal Background Records

Custom URL and Applications

State-Compliant Data

Address History

Identity Verification

Full Credit Report

VantageScore 3.0

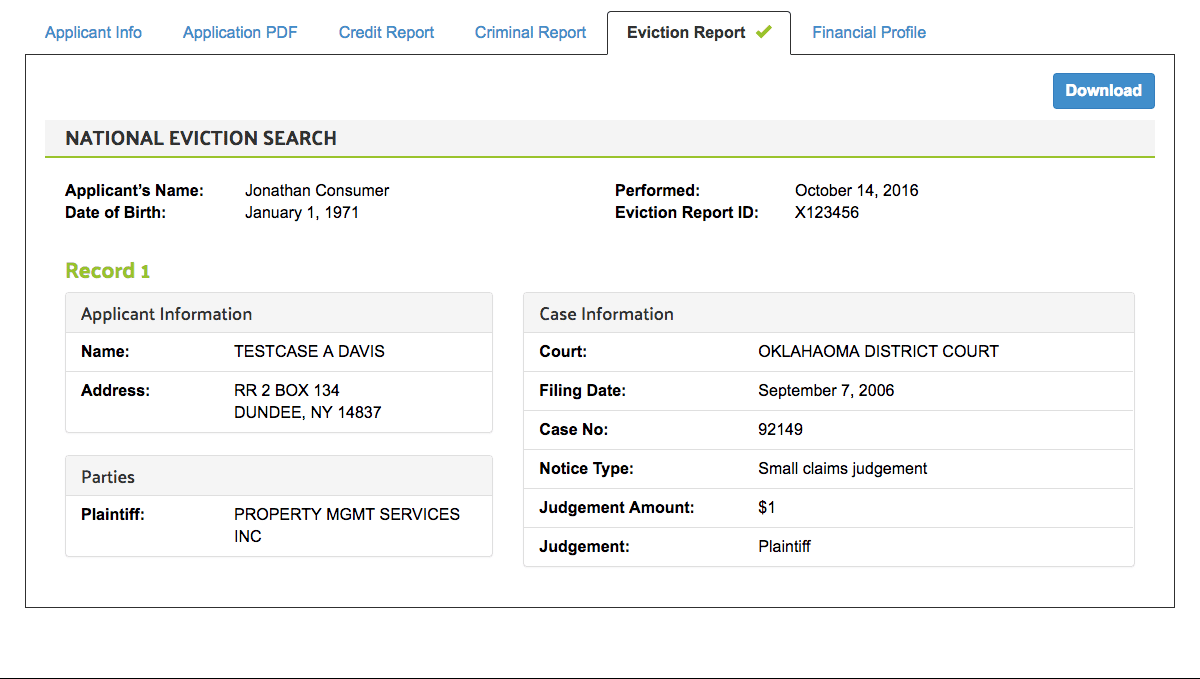

Eviction Records

Nationwide Eviction Database

Judgment Amount Details

Income Verification & Cash Flow Report

Payroll Deposits

Income & Expense Summary

Bank Account Balance

Discover More Features

FAQs

Frequently Asked Questions

A VantageScore credit of 650 or higher is considered good for tenant screening, indicating reliable financial behavior. LeaseRunner’s screening uses the VantageScore 3.0 model to provide accurate financial insights into potential tenants.

FICO and VantageScore 3.0 are both widely used credit scoring models, but they differ in how they calculate scores. VantageScore 3.0 uses a broader data set, including information from 36 million consumers who may have limited credit history, while FICO tends to focus on more traditional credit behaviors.

Many landlords rely on both FICO and VantageScore, but some landlords and property owners prefer VantageScore 3.0 for mortgage and tenant screening due to its broader data scope and ability to assess tenants with less credit history.